-

-

proud to

proud to

sponsor

-

-

Singapore officeBy opening an office in Singapore back in 2021

Singapore officeBy opening an office in Singapore back in 2021

we are signaling our growth ambitions in the APAC region. -

Trusted by the bestOur client base are asset managers, private equity firms, and hedge funds

Trusted by the bestOur client base are asset managers, private equity firms, and hedge funds

managing more than USD 35 trillion in assets,

representing a 35% market share of the world's largest 500 managers. -

-

London officeBy opening an office in London back in 2021

London officeBy opening an office in London back in 2021

we are signaling our growth ambitions in the UK market. -

Trusted by users worldwideUsers of our online market intelligence are located in 54 cities, 17 countries,

Trusted by users worldwideUsers of our online market intelligence are located in 54 cities, 17 countries,

10 time zones and 4 continents around the globe. -

-

Our missionSimply, to save our clients’ time, money and “nerves”,

Our missionSimply, to save our clients’ time, money and “nerves”,

and to empower them through comprehensive and accurate data and information. -

proud to

sponsor

-

Our digital servicesCloud-based consultant relations intelligence via our

Our digital servicesCloud-based consultant relations intelligence via our

NAVIGATION SYSTEM FOR CONSULTANT RELATIONS™. -

Our DNAAn independent service provider of data and market intelligence

Our DNAAn independent service provider of data and market intelligence

on truly institutional investment consultants.

Research approach and data integrity

TRULY GLOBAL RESEARCH ON INVESTMENT CONSULTING™

Research approach

Research is a semi-automated two-step process; it is a combination of digital-based research and handcrafted quality checks by our researchers.

In the first step research is conducted automatically by proprietary software and e-robotics like web-crawlers searching the worldwide web as well as external data extraction and relation software like text analytic APIs, tagging engines, deep learning software and other artificial intelligence software, e.g. OPEN CALAIS by Refinitiv [], IBM Watson, Google, apify.com, trackly.io among others. Our software and systems work around the world and around the clock in order to provide the information services that our clients have come to expect from us.

In the second step research is conducted manually by a team of researchers, all with academic background, permanently updating the database. The team enriches each dataset on the editor interface by combining data extracted from different sources, verifies the data by four-eyes principle and finally puts the data on the user interface visible for the end user.

Data sources

The business related data originates from publicly available and generally accessible sources, including company websites, company information providers, associations, the U.S. Securities and Exchange Commission (SEC), the Financial Conduct Authority (FCA) in the UK, social business networks, and news articles of digital publishing magazines. Sources of “Sensitive Personal Data” like Facebook, Instagram, Twitter, etc. are not included.

Data integrity

The basis to achieve a high level of data integrity is the daily maintenance of the data. Another fundamental step to assure a high accuracy and consistency of data is splitting the process of digital-based research from the manual verifying process on the editor interface and finally making the data visible on the user interface. Further technical and organizational measures are

- Database design with business relevant item data fields only

- Qualification and trainings of researchers

- Comprehensive maintenance manuals including data quality control rules and procedures

- Combining several different research tools

- Combining many different sources

- Integration of several online checking routines

- Four-eyes principle as a security precaution for approval of final disclosure to the end user

- Using several different email verification tools plus several different email finding tools

- Using writing apps and other quality assurance software

Research Papers

The Definition of Investment Consulting including Typology and Segmentation

Dr. Bastian Runge, 17 pp.

This paper provides a definition of the profession of investment consulting including a methodology for typology and segmentation. Starting with a general view on management consulting it explores the investment consulting as an independent professional advisory service. Next to the origins of the consulting profession and a description of the history of the consulting market it also gives an overview of the tasks, functions as well as roles of consultants.

Keywords: Investment consulting, management consulting, independent professional advisory service, problem solving, consulting tasks, consulting functions, roles of consultants, roots of modern consulting, history of the consulting market, origins of the consulting profession, typologization criteria.

The Definition of Investment Consulting including Typology and Segmentation

According to Steele ‘consulting’ is ”any form of providing help on the content, process, or structure of a task or series of tasks, where the consultant is not actually responsible for doing the task itself but is helping those who are.”[1]

A commission of experts in the USA has defined ‘management consulting’ as ”an independent and objective advisory service provided by qualified persons to clients in order to help them identify and analyze management problems or opportunities. Management consultants also recommend solutions or suggested actions with respect to these issues and help, when requested, in their implementation.”[2]

Kubr combines – in collaboration with an international circle of authors – the contents of these two definitions and concludes: ”Management consulting is an independent professional advisory service assisting managers and organizations to achieve organizational purposes and objectives by solving management and business problems, identifying and seizing new opportunities, enhancing learning and implementing changes.”[3]

The term ‘management consultant’ can be defined as “a universal term for any professional who provides assistance to others, usually for a fee.”[4]

All four definitions include the essence on which consulting is based: independent assistance with problem solving.[5] The existence of a problem is, thus, constitutive for a consulting demand.[6]

Unlike the expert who solves a problem on his own, the work of a consultant is characterized by interaction with the client in solving the problem.[7] This interaction is reflected, on the one hand, in the consultant’s understanding of the client’s affairs and, on the other hand, in the collaboration between consultant and client.

Moreover, the criterion of specialization in the expert sense is not sufficient since independence is another constitutive element of an external consultant: “Outside advisors brought specialized knowledge, not otherwise available, into organizations that faced problems that internal staff members could not easily resolve,” but “it is not their specialization that sets consultants apart but their continuing independence from the corporation.”[8]

In 1982, Turner presented a hierarchy of eight levels that illustrate the consulting tasks in a differentiated manner thereby contributing to an even more detailed definition:[9]

- Information conveyance

- Diagnosis of current state to redefine the problem

- Problem resolution

- Recommendations for action based on the diagnosis

- Implementation support

- Development of a joint understanding and commitment

- Support for organizational learning

- Permanent improvement of organizational effectiveness

According to Fink, management consultants ‘make’ management concepts. They invent the basic principles, design methods and instruments, and, that way, solve the problems of their clients.[10] Insofar, also knowledge transfer is, besides problem solving, a dominant function of consulting[11]; thus, knowledge is a central parameter in the definition of consulting.[12]

Besides law firms, auditing companies, and also investment banks, investment consultants are among ‘professional service firms’ that perform particularly knowledge-driven services.[13] Other functions that can be classified as latent are:

- Political function, i.e., use of a consultant to assert unshakeable notions and already a-priori made decisions.[14]

- Enforcement function, i.e., use of a consultant to support the achievement of a consensus in case of still variable notions and open decisions.

- Legitimation function, i.e., use of a consultant to block or at least reduce attribution of unfavorable or unpleasant developments to the management in charge.[15]

- Interpretation function, i.e., use of a consultant as (external) conversation and sparring partner to obtain new insights and perspectives through contemplation.

Regarding the political function of consultants, McKenna states that “administrators have employed outside advisors for thousands of years, but their counsel has traditionally been political, not commercial.“[16]

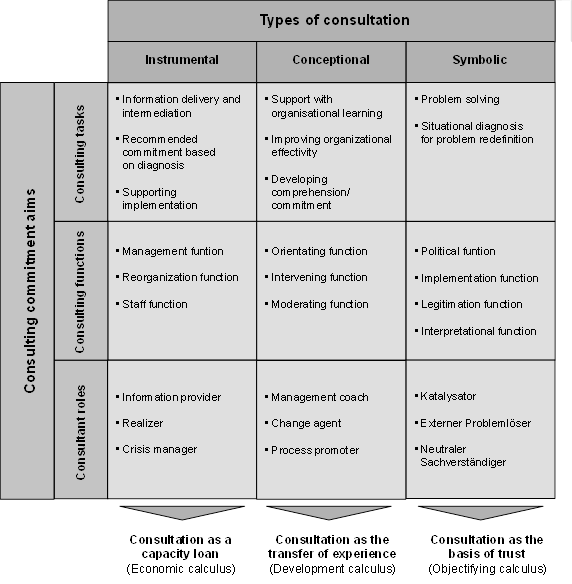

For a deeper understanding of consulting in general, it is advisable to take a look at the roles.[17] Since it is not expedient or even possible in the framework of this study to enumerate all the possible roles of consultants as “the list of roles is endless,”[18] the following figure offers an integrative observation of roles, functions, and tasks of consultants.[19]

Fig. 1: Tasks, functions, and roles of consultants. [20]

The term ‘investment consultant’ is not a protected professional title. This is also the reason for the lack of any official or generally recognized, clear and unequivocal definition. The U.S. Securities and Exchange Commission (SEC) subsumes investment consultants under the term ‘investment advisers:’ “A person that advises as to the selection or retention of an investment manager is considered an investment adviser”[21].

Yet, according to Mohe et al. the lack of a profession in the socio-professional sense […] does not necessarily [mean] the leave-taking from notions of professionalism as defined in a knowledge-sociological sense.[22]

Literally, the term ‘investment consultant’ refers to a consultant in matters of the asset side of a balance sheet. Consultants who are solely specialized in the analysis of the liability side and in actuarial consulting are, strictly speaking, called ‘pension consultants.’ The meaning, however, covers in fact a much wider scope than that.

If the term ‘management’ is replaced by ‘investment’, the above-mentioned definitions of management consulting largely provide a fitting template for a practice-oriented real definition[23] of investment consulting:

Investment consulting is

an independent professional consulting service,

which interactively – directly and as an intermediary –

supports institutional investors and their decision-makers

through solving investment problems

to optimally achieve their financial objects and goals

For systematic specification of the roles of investment consultants, the classification of the roles of management consultants according to Schein will be applied.[24] Investment consultants’ activities, as well as value-creation fields respectively, will be classified along those of management consultants and will be dealt with extensively and in a detailed manner in the following chapters.

In the framework of the ‘physician-patient relationship’ according to Schein, a customized solution is recommended following a comprehensive and detailed analysis of the client’s situation. In investment consulting, the following value creation steps must be attributed to that class: definition of investment policy, asset-liability analysis, and strategic asset allocation. With the ‘purchase of expertise’ according to Schein, the client makes use of the specific knowledge and expertise of the consultant in this area: These include such services as manager selection, allocation, and monitoring. In ‘process consulting’ according to Schein, consultants assist with their methodological competences, among them, services implementation as well as investment controlling.[25]

The essence of investment consultants’ classic roles – i.e., in the narrow sense[26] – is that “the role of the investment consultant is to manage, not to make investment decisions.”[27] In the same way the general roles of management consultants also apply to investment consultants, as do, by nature, the general functions. Investment consultant-specific functions pertaining to investment-related questions are the quality assurance function and the intermediation function.

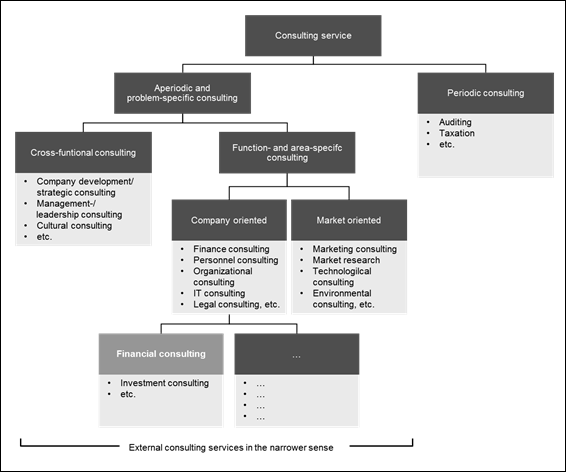

Through professional ‘screening’ as well as due diligence in the framework of manager selection, investment consultants reduce an information asymmetry that basically exists at all times, thereby contributing to an increase and respectively assurance of their clients’ quality of decisions. The intermediation function is the result of investment consultants being effectively active as ‘mediators.’ The following figure serves the classification of investment consulting within the context of various consulting services – and, thus, the distinction from other service types:

Fig. 2: Investment consulting within the context of various consulting services. [28]

This systematic classification and distinction enables an abstraction from the practice-oriented real definition and, that way, leads to a theory-oriented real definition of investment consulting:

Investment consulting is

an external,[basically aperiodic,] problem-specific and

function – resp. area-specific consulting service,

which represents a form of financial consulting for institutions.

through solving investment problems

to optimally achieve their financial objects and goals

Typology and Segmentation

The roots of modern consulting are in the USA[29] and can be traced back to the first half of the 19th century. Foster Higgins (1845), Sedwick (1858), and Arthur D. Little (1886) are considered to be the first consulting companies, whereby especially the latter is seen as the precursor of management consulting.[30]

In the 1820s, the choice of professional and external management services increased rapidly. A broad spectrum of options developed through consulting-related professions such as lawyers, accountants, and bankers. The profile of classic management consulting such as we know it today emerged only with the establishment of eventually world-renowned consulting companies such as Arthur Andersen (1913), Booz Allen Hamilton (1914), and McKinsey & Company (1926). Very beneficial in this context was the separation of commercial and investment banks through the Glass-Steagall Act of 1933. Until then, numerous tasks that nowadays are part of the core business of management consulting had been performed by commercial banks.[31] Besides the prohibition of emission of and trade with shares, this law also prohibited commercial banks to engage in business consulting and reorganization on behalf of their corporate customers.[32]

In the second half of the 20th century, further important consulting companies were founded such as The Boston Consulting Group (1963), Roland Berger (1967) as well as Bain & Company (1973). Also during that period, many consulting companies began to accelerate their internationalization and expanded their activities into Europe. US-American companies have been dominating the management consulting market worldwide ever since.

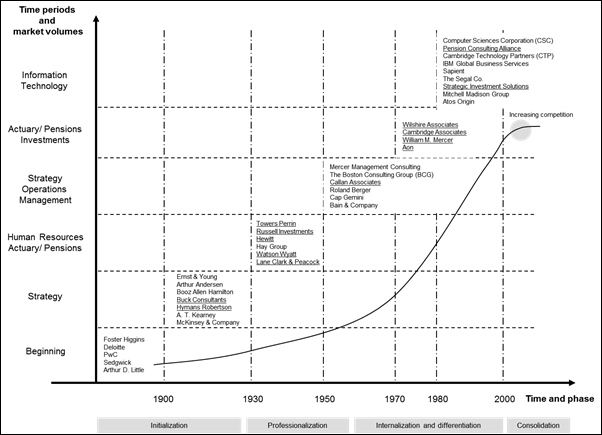

The following figure provides a chronological overview of the establishment of consulting companies in general and, thus, of the genesis and historical development of investment consulting:

Fig. 3: Founding years of important consulting companies. [33]

The above chronology of company foundations includes classic management consultants, consulting companies focused on auditing (cursive) as well as on pension and investment consultants (bold).

The history of how the consulting market evolved can be divided into three major periods, which represent the defining stages; these are: initialization, professionalization, internationalization, and concomitantly differentiation as well as consolidation. The following figure shows the attribution of investment consulting to periods and stages of the consulting market:

Fig. 4: Development periods and stages in the consulting market. [34]

The time before 1930 can be described as initialization since it was only then that today’s consultant profile evolved. The establishment of Buck Consultants (USA) and Hymans Robertson (UK), two investment consultants still active to this day, occurred already at that stage. The subsequent years into the 1960s are considered to be the professionalization stage since with increasing demand from industrial companies, methods and concepts kept developing. The term ‘management consultant’ took roots. The establishment of several investment consultants operating worldwide today falls in this stage: Russell Investments, Watson Wyatt[35] as well as Hewitt[36]. The 1970s were both the start of internationalization, which brought about the tapping of markets in Europe, Asia, and Latin America, and of differentiation, through which small consulting companies focusing on specific core areas evolved. In that phase from 1972 until 1982, a number of still operating US-American pension and investment consultants were founded: Callan Associates, Wilshire Associates, Cambridge Associates, William M. Mercer[37] as well as Aon[38]. Therefore, this decade can be described as the ‘cradle of modern investment consulting.’ Because of the increasing importance of computers, consulting companies specialized in information technology eventually evolved in the 1990s.

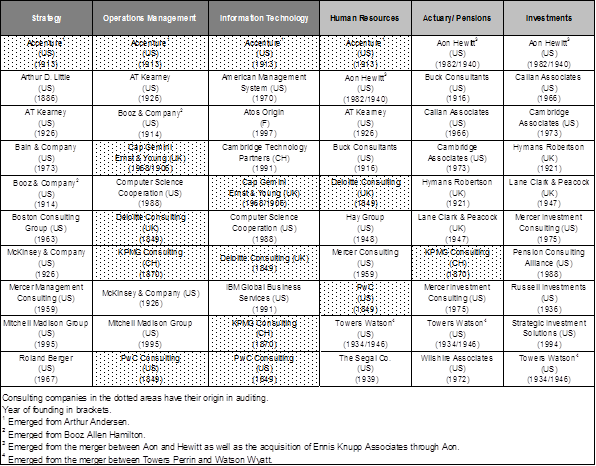

This grouping into periods, i.e., chronological clustering, can be fully converted into segments of homogenous types of consulting services, i.e., clustering according to content:

Fig. 5: The ‘Top 10’ consultants worldwide according to segments. [39]

The origins of the consulting profession are not just in management consulting in general, but, more specifically, also in strategic consulting (strategy). Later on, the consulting fields ‘operations management’ and ‘information technology’ developed.

From the above figure it becomes evident that most of the large traditional management consulting firms focus only on three activities. Thus, a ‘break’ can be discerned, which divides the segments into two halves[40]. The providers in the segments human resources, actuary/pensions as well as investments in the second half are to a large extent different firms from those in the first half.

Furthermore, it becomes apparent that several firms in the second half are among the ‘Top 10’ in several segments. Nevertheless, globally active firms originating mostly from the USA dominate both the first and second half. Myners states that investment consultants in the UK have gained market strength to a large extent based on their actuarial background.[41]

Moreover, it is notable that consulting units that are (PwC and KPMG) or were (Accenture[42]) part of an auditing company are active in the segments of both halves, but not in the fringe segments.[43] Nevertheless, the U.S. Securities and Exchange Commission (SEC) increased its pressure on auditing companies to part with their consulting units.[44] To bypass this requirement, all large firms preventively gave the business field ‘consulting’ a new designation, ‘advisory’. Also, there are no longer any ‘consultants’, instead there are ‘advisors’.[45]

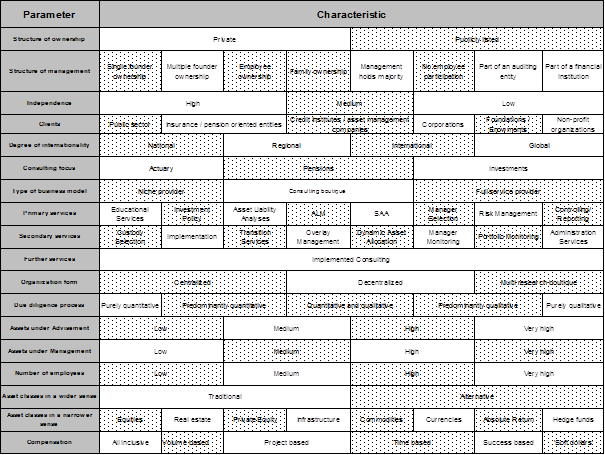

To achieve the typologization and segmentation of an individual investment consultant, it again makes sense to point out the possibility of a schematical classification. After all, the scope of individual characteristics is – like in asset management companies – extremely varied. Individual characterization is possible based on the morphological box below:

Fig. 6: Typologization criteria of investment consultants. [46]

References

Binnewies, S. (2002)

(Strategisches Management professioneller Dienstleistungen am Beispiel der Unternehmensberatung):

Strategisches Management professioneller Dienstleistungen am Beispiel der

Unternehmensberatung, Göttingen, Duehrkohp & Radicke.

Biswas, S./ Twitchell, D. (2002) (Management Consulting: A Complete Guide to the Industry): Management Consulting:

A Complete Guide to the Industry, 2nd Edition, New York, New York, John Wiley

& Sons.

Bloomfield, B. P./ Danieli, A. (1995) (The Role of Management Consultants): The Role of Management

Consultants in the Development of Information Tech-nology, Journal of

Management Studies, Vol. 32, Hoboken, New Jersey, Wiley-Blackwell, S. 23-46.

Bower, M. (1982) (The Forces That Launched Management Consulting Are Still at Work): The Forces That

Launched Management Consulting Are Still at Work, Journal of Management

Consulting, Vol. 1, No.1, S. 4-6.

Canbäck, S. (1998) (The Logic of Management Consulting – Part 1): The Logic of Management Consulting –

Part 1, Journal of Management Consulting, Vol. 10, No. 2, Institute of

Management Consultants, New York, New York, S. 3-11.

Caroli, T. S. (2007) (Unternehmensberatung als Sicherstellung von Führungsrationali-tät?):

Unternehmensberatung als Sicherstellung von Führungsrationalität? In: Nissen,

V. (Hrsg.): Consulting Research – Unternehmensberatung aus wissenschaftlicher Perspektive,

Wiesbaden, Deutscher Universitäts-Verlag, S. 109-126.

Ernst, B./ Kieser, A. (2002) (In Search of Explanations for the Consulting Explosion): In Search of

Explanations for the Consulting Explosion. In: Sahlin-Andersson, K./ Engwall,

L. (Eds.): The Expansion of Management Knowledge, Stanford, Stanford Business

Book, S. 47-73.

Faust, M. (1998) (Die Selbstverständlichkeit der Unternehmensberatung): Die Selbstverständlichkeit

der Unternehmensberatung. In: Howald, J./ Kopp, R. (Hrsg.): Sozialwissenschaftliche

Organisationsberatung: Auf der Suche nach einem spezifischen

Beratungsverständnis, Berlin, Ed. Sigma, S. 147-181.

Fink, D. (2003) (Managementansätze im Überblick): Managementansätze im Überblick. In: Fink, D.

(Hrsg.): Management Consulting Fieldbook: Die Ansätze der großen

Unternehmensberater, 2., überarbeitete und erweiterte Auflage, München, Vahlen,

S. 13-24.

Fink, D. (2005) (Machiavelli, McKinsey & Co.): Machiavelli, McKinsey & Co. – eine kleine Geschichte

der Managementberatung. In: Petmecky, A./ Deelmann, T. (Hrsg.): Arbeiten mit

Managementberatern – Bausteine für eine erfolgreiche Zusammenarbeit, Berlin –

Heidelberg – New York, Springer, S. 189-203.

Franck, E./ Pudack, T./ Benz, M.-A. (2003) (Unternehmensberatung als Legitimation): Unternehmensberatung als

Legitimation, Working Paper No. 21, Working Paper Series ISSN 1660-1157,

Zürich, Universität Zürich.

Gattiker, U. E./ Larwood, L. (1985) (Why Do Clients Employ Management Consultants?): Why Do Clients

Employ Management Consultants?, Human Science Press, S. 120-129.

Gummesson, E. (2000) (Qualitative Methods in Management Research): Qualitative Methods in Management

Research, 2nd Edition, Thousand Oaks, California, Sage Publications.

Heuermann, R./ Herrmann, F. (2003) (Hrsg.) (Unternehmensberatung): Unternehmensberatung – Anatomie und

Perspektiven einer Dienstleistungselite, München, Vahlen.

Kennedy Consulting Research & Advisory (2010) (Consulting Capability Assessments): Consulting

Capability Assessments, http://www.kennedyinfo.com/ consulting/analystservices

/assessments?C=vcRUNkJ5kxwYW0bk&G=qzITtFX263wsHqwC, Peterborough, New

Hampshire.

Kieser, A. (1998) (Unternehmensberater): Unternehmensberater – Händler in Problemen, Praktiken

und Sinn. In: Glaser, H./ Schröder, E./ v. Werder, A. (Hrsg.): Organisation im

Wandel der Märkte, Wiesbaden, Gabler, S. 192-225.

Kleeberg, J. M./ Schlenger, C. (2000) (Die Rolle von Consultants im Rahmen der Spezialfondsanlage): Die Rolle

von Consultants im Rahmen der Spezialfondsanlage. In: Kleeberg, J. M./

Schlenger, C. (Hrsg.): Handbuch Spezialfonds: Ein praktischer Leitfaden für

institutionelle Anleger und Asset Management Gesellschaften, Bad Soden/Ts.,

Uhlenbruch, S. 871-897.

Kraus, S./ Mohe, M. (2007) (Zur Divergenz ideal- und realtypischer Beratungsprozesse): Zur Divergenz ideal- und

realtypischer Beratungsprozesse. In: Nissen, V. (Hrsg.): Consulting Research –

Unternehmensberatung aus wissenschaftlicher Perspektive, Wiesbaden, Deutscher

Universitäts-Verlag, S. 263-279.

Kromrey, H. (2009) (Empirische Sozialforschung): Empirische Sozialforschung, 12., neu bearb.Auflage,

Stuttgart, UTB.

Kubr, M. (Ed.) (2002) (Management Consulting: A Guide to the Profession): Management Consulting: A

Guide to the Profession, 4th Edition, Geneva, International Labour Office.

Maister, D. (2010) (Professionalism in Consulting): Professionalism in Consulting. In: Greiner,

L./ Poulfelt, F. (Eds.): Management Consulting Today and Tomorrow: Perspectives

and Advice from 27 Leading World Experts, New York – London, Routledge.

McKenna, C. D. (1995) (The Origins of Modern Management Consulting): The Origins of Modern Management

Consulting, Business and Economic History, Vol. 24, No. 1, S. 51-58.

McKenna, C. D. (2006) (The World’s Newest Profession): The World’s Newest Profession: Management Consulting

in the Twentieth Century (Cambridge Studies in the Emergence of Global

Enterprise), Cambridge, Cambridge University Press.

Mohe, M./ Heinecke, H. J./ Pfriem, R. (2002) (Beratung als Geschäft): Beratung als Geschäft. In: Mohe, M./

Heinecke, H. J./ Pfriem, R. (Hrsg.): Consulting – Problemlösung als

Geschäftsmodell – Theorie, Praxis, Markt, Stuttgart, Klett Cotta, S. 221-224.

Myners, P. (2001) (Institutional Investment in the United Kingdom: A Review): Institutional

Investment in the United Kingdom: A Review, London, HM Treasury.

Nees, D. B./ Greiner, L. E. (1985) (Seeing Behind the Look-Alike Management Consultants): Seeing Behind the

Look-Alike Management Consultants, Organisational Dynamics, Vol. 13, Elsevier,

S. 68-79.

Niedereichholz, C./ Niedereichholz, J. (2006) (Consulting Insight): Consulting Insight, München – Wien, Oldenbourg.

Niewiem, S./ Richter, A. (2007) (Make-or-buy Entscheidungen für Beratungsdienstleistungen): Make-or-buy

Entscheidungen für Beratungsdienstleistungen – Eine empirische Untersuchung.

In: Nissen, V. (Hrsg.): Consulting Research – Unternehmensberatung aus

wissenschaftlicher Perspektive, Wiesbaden, Deutscher Universitäts-Verlag, S.

57-72.

Pensions & Investments (2010) (Research Center): Research Center, http:// www.pionline.com, Crain

Communications Inc., Detroit, Michigan, [accessed on November 12, 2010].

Poulfelt, F./ Greiner, L./ Bhambri, A. (2010) (The Changing Global Consulting Industry): The Changing

Global Consulting Industry. In: Greiner, L./ Poulfelt, F. (Eds.): Management

Consulting Today and Tomorrow: Perspectives and Advice from 27 Leading World

Experts, New York – London, Routledge, S. 5-32.

Schein, E. H. (1988) (Process Consultation Vol. 1): Process Consultation Vol. 1: Its Role in

Organisation Development, 2. Auflage, Reading, MA, Addison-Wesley.

Steele, F. (1981) (Consulting for Organizational Change): Consulting for Organizational Change,

Amherst, Massachusetts, University of Massachusetts Press.

Sturdy, A. (1997) (The Dialectics of Consultancy): The Dialectics of Consultancy, Critical

Perspectives on Accounting, Vol. 8, S. 511-535.

Thomson Nelson (2010) (Database): Database, http://www.nelsoninformation. com, Thomson Reuters, New

York, New York.

Trone, D./ Allbright, W./ Taylor, S. (1996) (The Management of Investment Decisions): The Management of

Investment Decisions, New York, New York, McGraw-Hill.

Turner, A. N. (1982) (Consulting Is More Than Giving Advice): Consulting Is More Than Giving Advice,

Harvard Business Review, Vol. 60, September-October, Boston, Massachusetts,

Harvard Business Publishing, S. 120-129.

U.S. Securities and Exchange Commission (SEC) (2004) (Investment Advisers Act of 1940): Investment

Advisers Act of 1940, Revised through September 2004, Washington, D.C.

Wilkinson, J. W. (1995) (What

is Management Consulting?): What is Management Consulting? In: Barcus, S. W./

Wilkinson, J. W. (Eds.): Handbook of Management Consulting Services, New York,

New York, McGraw-Hill, S. 1-3 bis 1-16.

Ziegler, A. (1995) (Beratung

beim Wort genommen): Beratung beim Wort genommen. In: Wohlgemuth, A. C./

Treichler, C. (Hrsg.): Unternehmensberatung und Management: Die Partnerschaft

zum Erfolg, Zürich, Versus, S. 55-65.

Footnotes

[13] See Kraus/ Mohe (2007): Zur Divergenz ideal- und realtypischer Beratungsprozesse, p. 271.

Investment Consulting in Institutional Asset Management – Table of Contents

Conceptual Design and Empirical Analysis from a Global Perspective with Particular Focus on Manager Selection

Dr. Bastian Runge, 520 pp.

This research paper provides a holistic analysis of investment consulting as an important service segment in institutional asset management. Its subject is the theoretical and empirical analysis of supply, demand, market environment and the interactions between market participants in investment consulting. The focus is on manager selection as a substantial part of the business model and value chain. It provides a definition of the profession as an independent professional advisory service including a methodology for typology and segmentation. Next to the origins of the consulting profession it gives an overview of the tasks, functions as well as roles of consultants. This paper also contains an empirical analysis of the supply in investment consulting from a worldwide perspective. It differentiates between the regions Americas, EMEA and APAC as well as the Anglo-Saxon and the non-Anglo-Saxon regions. The business model and value chain are analyzed by comparing the supply and demand of services according to asset categories, by presenting a SWOT analysis of exogenous and endogenous factors, and by presenting various compensation models.

Keywords: Investment consulting, definition and scope, typology and segmentation, market size and structure, defining dimensions of demand, scientific components of explanation, information economics, transaction cost theory, property rights theory, principal agent theory, concept of fiduciary, concept of trusteeship, service components of supply, business model and value chain, definition of investment policy, asset-liability analysis, strategic asset allocation, manager selection, allocation, and monitoring, implementation, investment controlling, due diligence, process and instruments of manager selection, databases, request for proposal (RFP), research interview, on-site visit, beauty contest, criteria of manager selection, 6-P approach (people, philosophy, process, performance, product, pricing), exogenous and endogenous trends and drivers, selection of investment consulting providers, dealing with providers in investment consulting, quantitative and qualitative value-added by investment consulting, implications for practice.

Defining Dimension of Demand for Investment Consulting – Scientific Components of Explanation

Dr. Bastian Runge, 27 pp.

In many aspects, the demand for investment consulting can be explained by phenomena investigated in the theories of the new institutional economics. Significant drivers of demand are information risks, delegation risks and problems resulting thereof, such as asymmetrical information distribution, asymmetrical assessment and asymmetrical competence regarding problem-solving. These problems can be mitigated by the intermediatory function of investment consultants. These theoretical phenomena can also be found in practice in investment consulting and therefore are of high relevance for the actual market participants. They constitute the next major challenge in the asset management industry as a whole.

Keywords: Investment consulting, delegated portfolio management, improving the efficiency of coordination and exchange processes, neo-institutional explanatory approach, new institutional economics, information economics theory, transaction cost theory, property rights theory, principal agent theory, information asymmetry, adverse selection, hold-up, moral hazard, hidden information, hidden characteristics, hidden intention, hidden action, signaling, screening, reputation building, incentives, monitoring.

The Supply in Investment Consulting – Empirical Analysis of Business Model and Value Chain

Dr. Bastian Runge / David P. Pfleger, 13 pp.

This paper provides an empirical analysis of the supply in investment consulting from a worldwide perspective. It differentiates between the regions Americas, EMEA and APAC as well as the Anglo-Saxon and the non-Anglo- Saxon regions. The business model and value chain are analyzed by comparing the supply and demand of services according to asset categories, by presenting a SWOT (strengths, weaknesses, opportunities and threats) analysis of exogenous and endogenous factors, and by presenting various compensation models. Exogenous are facts that influence investment consulting externally, i.e. through the asset management business, while endogoenous drivers influence this market segment from an internal point of view.

Keywords: Investment consulting, business model and value chain, manager selection and its process, instruments and criteria, self-image of investment consultants, SWOT analysis of exogenous and endogenous factors including consulting-barbell, convergence of asset management and investment consulting, implemented consulting and fiduciary management as well as consultants for investment consultants (meta-consultants), compensation models in investment consulting.

Leadership team

TaunusTurm |

Phone

Google Maps ![]()

London W1J 8LQ | United Kingdom

Phone

Google Maps ![]()

Chicago, IL 60606 | USA

Phone

Google Maps ![]()

Singapore 189720 | Singapore

Phone

Google Maps ![]()

Peter Brackett, ASIP | London

Copyright © 2014 – 2024 │ IC Research Institute │ Privacy Policy │ Legal Information and Disclaimer